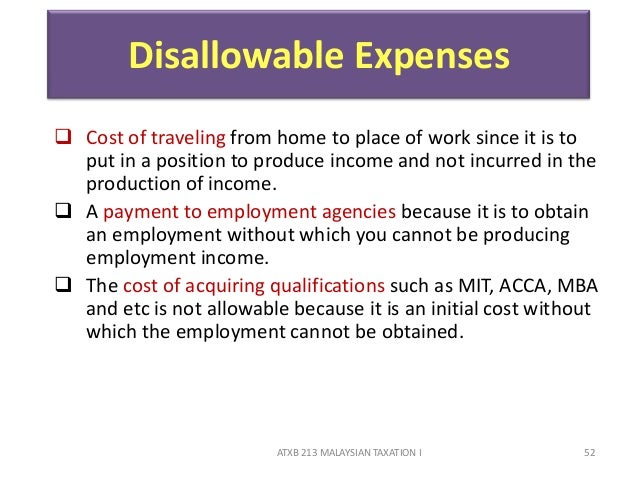

Non Allowable Expenses For Corporation Tax Malaysia

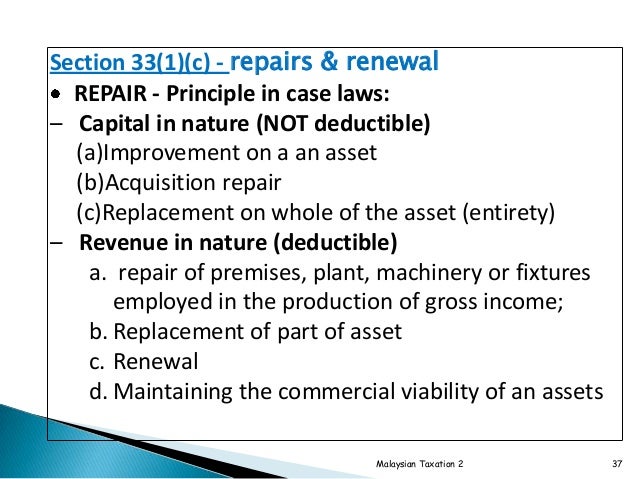

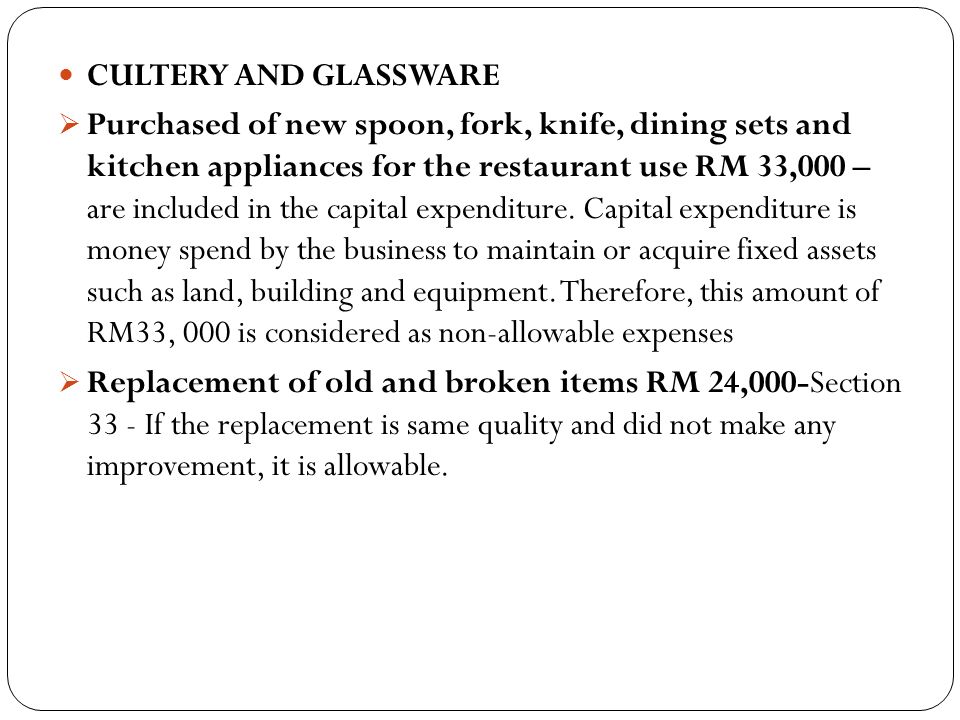

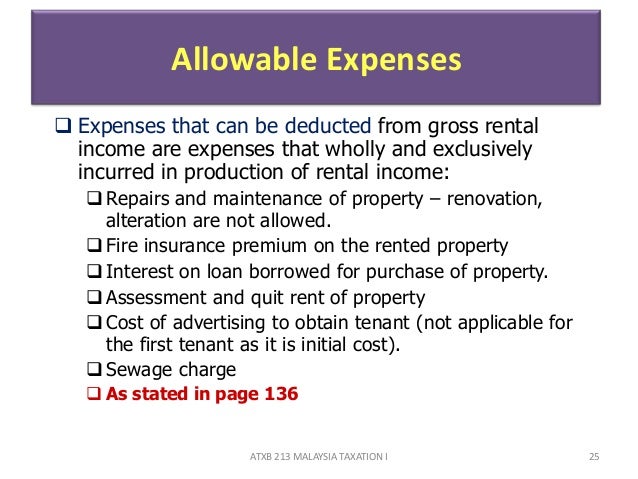

Expenses on repairs and renewals generally repairs and renewals expenses are claimed as deductions from a person s gross income from a business or rental source.

Non allowable expenses for corporation tax malaysia. Staff entertaining is an allowable expense for company tax purposes whereas client entertaining may be an allowable expense and a portion may be disallowed for company tax purposes. Malaysia corporate taxes on corporate income last reviewed 01 july 2020. 6 3 annual corporate filings and meeting expenses a secretarial fees.

It is frequently unclear whether a certain tax expense might qualify as a tax deduction or not. 6 4 income tax returns a cost of filing of tax returns and tax computations. B annual general meeting expenses.

And if you deduct an expense that doesn t qualify you might be faced with a tax notice or tax audit. A company or. 6 5 legal expense incurred by a landlord.

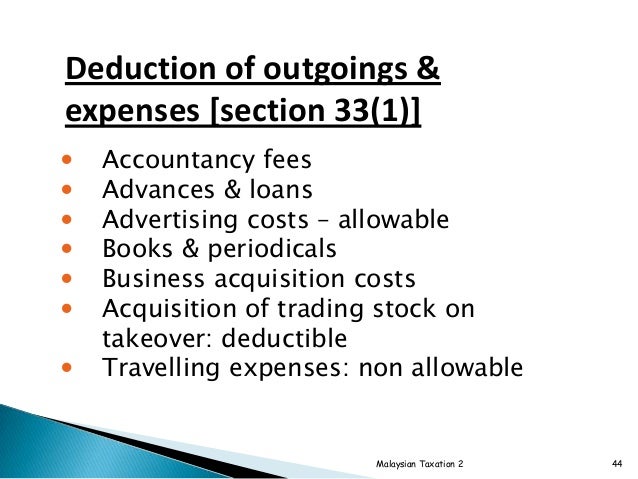

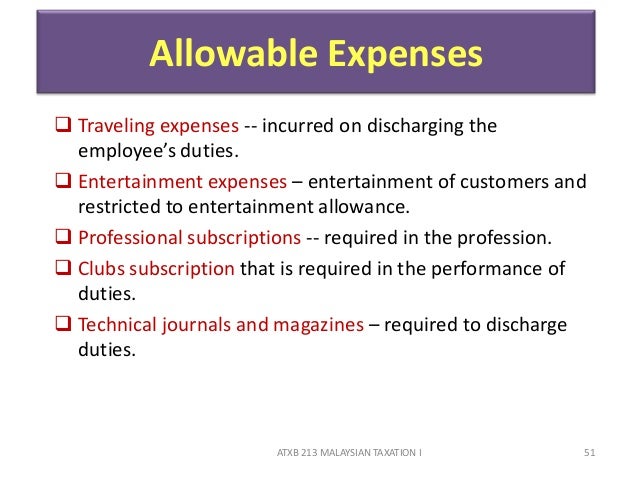

Allowable business expenses. Knowing what expenses are not tax deductible might help company to minimise such expenses. Legal fees are usually allowable and this includes costs of chasing debts defending trademarks preparing legal agreements.

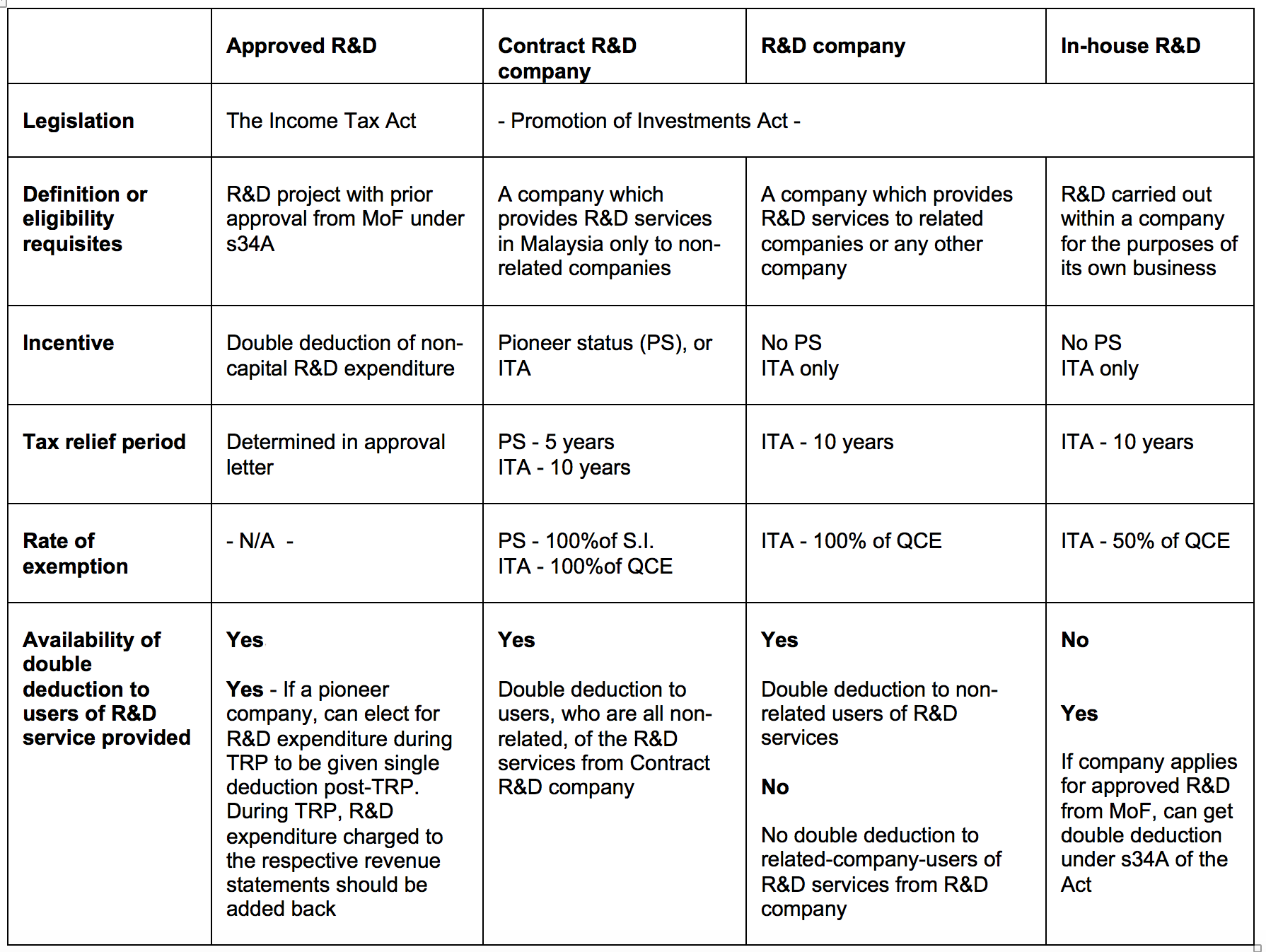

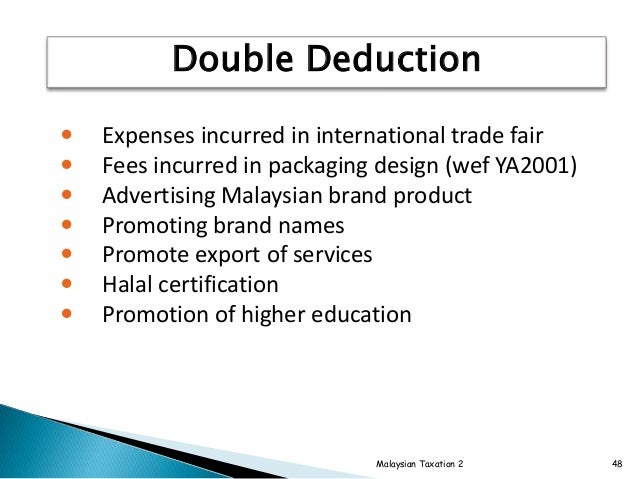

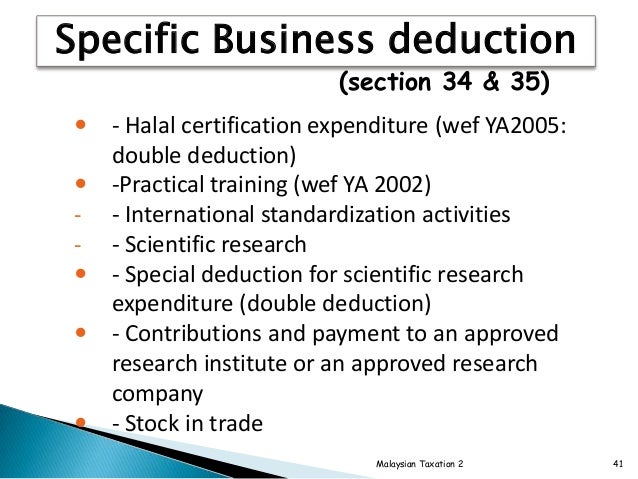

A non tax deductible expense is a purchase that does not facilitate the normal operation of your business and cannot be used to offset tax costs. Allowable specific expenses double deduction expenses allowable under income tax act 1967. Often it is obvious which expenses are deductible and which aren t.

Our malaysia corporate income tax guide. Fortunately there are many deductible tax expenses that exist so you may be surprised that your tax expense of choice qualifies for a tax deduction. For both resident and non resident companies corporate income tax cit is imposed on income accruing in or derived from malaysia.

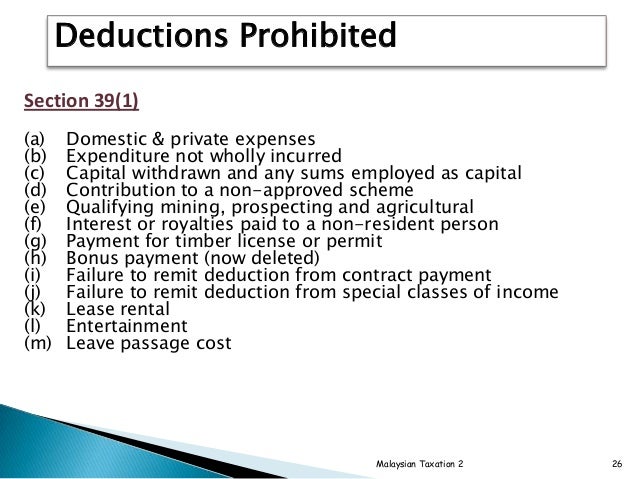

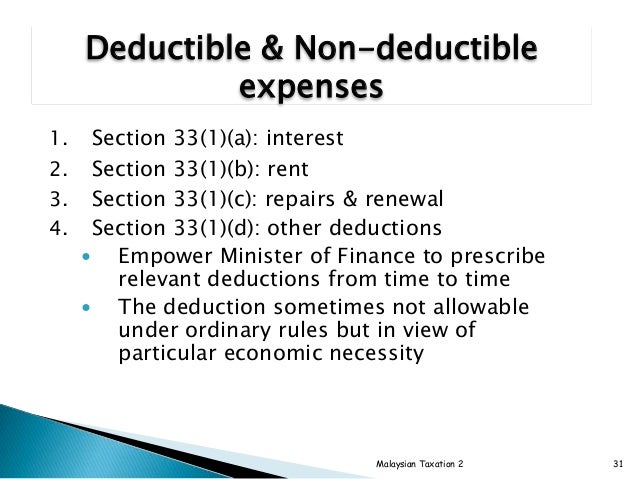

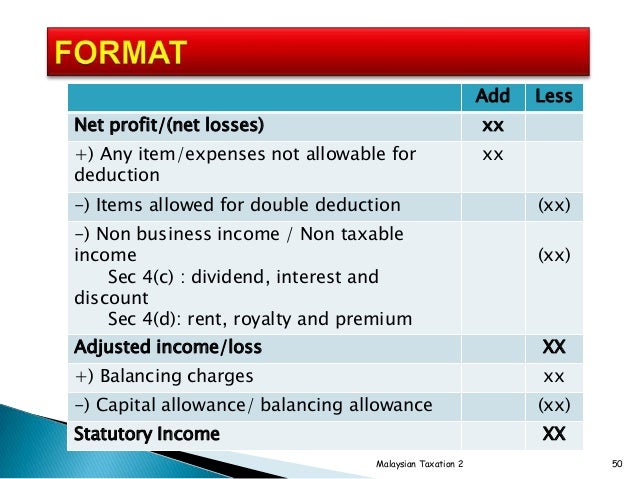

Corporate income tax in malaysia is applicable to both resident and non resident companies. Adjusted income from business source is derived from gross income after deduction of business expenses such as. However the allowable expenses under subsection 33 1 of the ita is subject to specific prohibitions under subsection 39 1 of the ita.

Nondeductible tax deductions expenses. Interest expense is allowed as a deduction if the expense was incurred on any money borrowed and employed in the production of gross income or laid out on assets used or held for the production of gross income. B cost of appeal against income tax assessment i e.

To the special commissioners of income tax and the courts. Companies are taxed at the 24 with effect from year of assessment 2016 while small scale companies with paid up capital not exceeding rm2 5 million are taxed as follows. The following are more common non allowable expenses.

The proportion of interest expense will be allowed against the non business income. The current cit rates are provided in the following table. Export allowances business expenses.

Legal and professional fees.

.jpg)